Content

- 1. Importance of sustainable finance for member institutions and implementation examples

- 2. Overview of the sustainable finance framework and activities of the Association of German Banks

- 3. Outlook

The years 2020 and 2021 have shown that sustainability and climate change are the burning issues of our time and have had an impact on the financial sector for some time now. Sustainable finance, the transformation to a carbon-neutral economy, social development goals – all these topics have become more important in the social discourse and, at the same time, are having an increasing impact on the strategic orientation of private banks.

The private banks are already incorporating a variety of sustainability topics into their core business and making a considerable contribution to answering the pressing questions of the day when it comes to sustainable finance. It has becoming increasingly clear that:

Private banks see themselves as responsible for shaping the transformation and are supporting their customers to ensure they still have viable business models even in 20 years’ time.

A representative forsa survey conducted in cooperation with the Association of German Banks from 2021 [1] has shown that corporate customers appreciate this.

The first ever position paper by the private banks on the topic of sustainability/sustainable finance in 2020 [2] received excellent feedback across the finance sector and beyond. We aim to use this momentum to further increase the visibility of the activities being implemented [3] by the private banks in this area.

This report presents the Association of German Banks’ commitment to sustainable finance and highlights the topics relevant to this issue. It provides an overview of the regulatory framework, shows the high status of sustainable finance among member institutions of the association and outlines example of how some activities are being implemented. This report is a continuation of the position paper from 2020 and provides a revealing insight into the progress achieved and hurdles encountered so far.

1. Importance of sustainable finance for member institutions and implementation examples

Following on from last year’s survey of member institutions, the Association of German Banks again asked its members about their approach to sustainable finance in 2021. A total of 41 institutions took part, representing almost one quarter of all member institutions. The new survey findings reinforced impressions gained from the previous year: sustainability is a strategic topic and of key importance to the institutions. Key focus areas for the near future are the implementation of the EU taxonomy, the further development of ESG (environment, social and governance) reporting and taking into account ESG risks.

1.1 Strategic view

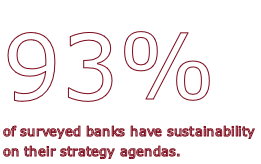

Many key findings from the survey clearly show that sustainability is an important issue for banks today and will only continue to gain importance in the future. For example, 93% of surveyed banks have either integrated sustainability into their overall strategies or have a sperate sustainability strategy on their agendas. And 71% have included ESG risks in their business strategies.

Nearly half of all surveyed institutions (43 %) indicated that sustainability plays an important or very important role in their overall strategies. According to their estimates, this will be the case for 85% of banks surveyed in five years. For comparison: in 2020, 19% of surveyed banks named sustainability as a very important topic; 65% thought it would be in five years.

An evaluation of the responses by size of institution gives us an even clearer picture: 29% of small banks indicated that sustainability now plays an important or very important role in their overall strategies. In five years, this would be the case for 71% of small banks.

As was the case in 2020, there are a number of reasons for banks to address sustainability; alongside regulation (90%), risk management also plays an important role here (80%). However, the institutions made it clear they want to take on the social responsibility of addressing the issues surrounding sustainability (80%). 78% of respondents saw sustainability as important for the reputation of their institution. While 76% saw society as the driver of sustainability (52% in 2020), 73% of surveyed members also saw sustainability as a business opportunity.

It remains the case that voluntary commitments are a relevant strategy for private banks wishing to engage in this issue. Measured in terms of the total assets of all private banks, 78% of our institutions have signed up to at least one commitment related to sustainability.

1.2 Future topics

Sustainability and, in particular, combatting climate change could soon have a massive impact on the financial sector. Our member institutions also assume that the effects of global warming will soon have a tangible impact on their own business. 45% stated that they anticipate experiencing relatively strong to strong effects from climate change in the next five years.

The goals of the Paris Climate Agreement are the cornerstones of global efforts to mitigate the effects of climate change and also act as guiding principles for the financial sector. 40% of member institutions have defined concrete measures that are linked to the Paris climate goals, especially the larger banks.

In addition, 34% of respondents indicated they were carrying out concrete measures to implement the Sustainable Development Goals (SDGs), compared to 23% in 2020.

Member institutions will focus on the following in the coming months:

- Further developing their sustainability strategies

- Implementing the EU taxonomy for sustainable investments

- Further developing their reporting procedures

- Communicating with their customers on sustainability

- Aligning with the Paris Climate Goals

- Calculating and reducing CO2 emissions

- Defining climate and environmental key figures of their corporate customers

- Taking account of human rights

These are all linked to a variety of processes not listed in detail here, such as creating portfolio transparency and assessing conformity with the EU taxonomy.

Taking a more differentiated view, if we divide our responses according to size of bank, the study reveals that for 70% of small banks drawing up a sustainability strategy is either important or very important. For the larger banks, the implementation of the requirements of the EU taxonomy are their priority. 85% of respondents thought this topic was either important or very important.

1.3 Securities and lending business

Our study shows that sustainability is playing an increasingly important role in the customer/bank relationship. More than half of the institutions (56%) said that this topic was now being actively discussed in client meetings concerning loans. At nearly half (49%) of all banks surveyed, the topic of sustainability was frequently discussed in client meetings. And 7% of respondents even went on to say that clients bring up the subject of sustainability in nearly all meetings. Nevertheless, 22% said that clients seldom wanted to discuss sustainability.

What aspects in particular do clients want to discuss? 79% of institutions stated that clients ask about support programmes for more sustainability. In order to better address the wishes of their clients, our member institutions are calling for public sustainability support programmes to be more transparent. Making them less complex would be advantageous for both clients and financial institutions.

When it comes to securities business, there has been increased demand for green bonds in particular (71%) – we estimate this demand has largely come from institutional customers. Member institutions have also recognised a trend towards sustainable investment funds (76%); this is more likely to have come from private customers.

In relation to securities business, member institutions noticed a rising demand for sustainable securities services. While in 2020, 13% of banks identified a considerable increase in demand, this figure jumped to 29% in 2021. 54% of respondents observed

a moderate increase in demand for such services.

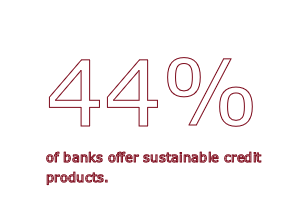

There was also a noticeable trend towards more sustainability when it came to credit products. While in 2020, 37% of institutions were able to offer their retail and corporate customers sustainable credit products, in 2021, 44% of institutions had included these credit products in their range (for large banks this figure was even higher: 70% of respondents). Sustainable credit products are mostly being offered to companies (43% to big companies and 32% to SMEs). Overall, 40% of respondents indicated that the proportion of loans in corporate portfolios explicitly linked to sustainability criteria was at least 5%. Nearly 80% of respondents estimated that this figure would rise to at least 10% in five years.

The proportion of sustainable ecological activities on the loan books of our survey participants is currently at a maximum of 10% for 71% of respondents. These figures will certainly change. Only 25% of banks expect the proportion of ecologically sustainable activities to be less than 10% of their entire portfolios in five years’ time. It is important to note, however, that the taxonomy, which will act as a classification framework for ecologically sustainable economic activities, has yet to be finalised. Banks are in the process of examining the taxonomy in detail. The first so-called green asset ratios are due to be developed in 2022. This will be an intensive process with many prerequisites. A broad discussion process is expected in order to evaluate and contextualise these targets.

Member institutions also expect that the proportion of loans in a banks’ corporate portfolio with an explicit link to sustainability criteria is also likely to increase in the coming years.

1.4 Risk management

The inclusion of ESG risks in risk management processes is also gaining pace. Three quarters (75%) of surveyed institutions already include environment, social and governance risks in their risk strategies, with major banks further ahead on 90%. 65% of small banks said they incorporate ESG risks in their business and risk strategies.

In addition, nearly 30% of respondents were currently measuring, monitoring and managing climate risks. Again, this figure has increased over that of 2020. As many as 68% of those surveyed took account of ESG factors in their credit analyses.

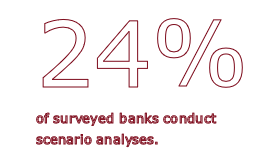

Furthermore, many institutions are addressing scenario analyses on sustainability risks; nearly 25% of respondents are already implementing these today. Due to the often very long timeframes involved, e.g. in the case of climate risks and the corresponding complexity of the transmission channels, scenario analyses are anything but trivial. This might explain the differences seen between large and small banks: 45% of larger institutions conduct scenario analyses, but only 5% of small institutions do.

72% of banks that conduct analyses said they would use the findings to develop recommendations and use them to improve their processes. Furthermore, 22% of surveyed institutions stated that they had increased their capital cover as a result of having taken a more in-depth approach to scenario analyses.

1.5 Reporting

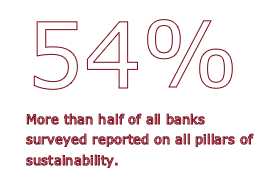

Sustainability reporting continues to be an important topic for banks. What is the reporting about? 54% of respondents are currently already providing information on all three pillars of sustainability (environment, social and governance). Of those institutions providing comprehensive reports on climate and environmental topics, 31% focus on sustainable financing, 21% on concrete environmental and climate goals and 20% on ESG risks.

Around 62% of surveyed institutions assume that in five years there will be comprehensive reporting on qualitative goals. And there is a similar pattern with quantitative goals: 61% expect them to be included extensively in their reporting.

A further indicator of the importance of sustainability for institutions: Around 43% of surveyed institutions said that sustainability is reported to their executive committees and/or managing directors. Some banks have even set up high-level management committees.

However, the formats of those reports vary: Of the respondents who report on sustainability, half prepare an independent sustainability report, while a quarter integrate sustainability completely into their management reports or have added a separate section to their management reports.

2. Overview of the sustainable finance framework and activities of the Association of German Banks

Transformation towards more sustainability is a necessity – there is no question about it: not acting is not an option for the private banks. In 2021, a number of regulatory measures and initiatives in the area of sustainable finance have already been discussed and launched; further developments are expected shortly.

2.1 Private banks in dialogue

Interest in sustainability is growing rapidly among customers, lawmakers, investors, supervisors and private banks. This also increases the demand and need to develop points of view and find joint solutions.

Focus on sustainability at the German Banking Congress

In April 2021, the Association of German Banks made sustainability a focus of its triennial German Banking Congress. As a panel of experts highlighted, sustainability is not a niche issue and it is beyond dispute that a sustainable economy must be our goal. The panellists nevertheless believed action was essential. They saw a need for a consistent political framework that would help all involved make swifter progress on climate policy. Banks must remain capable of acting instead of being swamped by regulation overload. And further incentives for sustainable business models and a more sustainable financial market were necessary.

Numerous exchanges of practical experience and learning forums

This flagship event was complemented by a lively exchange with businesses in the real economy and associations on topics such as practical experience with the EU taxonomy of environmentally sustainable economic activities. This has given businesses and banks

a better understanding of how the as yet new Taxonomy Regulation should be applied.

Through the Banking Academy, the Association of German Banks has organised webinars to promote greater understanding of selected sustainability issues like the Transparency Regulation, ESG risks and the obligation for banks to carry out human rights due diligence.

Sustainable finance – with the focus on people

The private banks are gradually making sustainability part of their core business. The Association of German Banks has recorded a video series of conversations with some of its members about sustainability in the banking world. These thought-provoking discussions with sustainable finance experts from our member banks can be found at www.bankenverband.de during COP26 (in German).

A look at the real economy: transformation is seen as an opportunity too

In cooperation with OMFIF, the Official Monetary and Financial Institutions Forum, the Association of German Banks in 2021 helped to develop a representative forsa survey of 104 SMEs and 32 listed companies with 250 or more employees. The project was conducted under the auspices of the German Federal Ministry of Finance and the Embassy of the Grand Duchy of Luxembourg. Key findings of the study, which was unveiled on 17 June 2021: next to overcoming the consequences of the coronavirus crisis, sustainability will pose the greatest challenge for SMEs over the next twelve months. Many companies expect the time and effort involved in applying for conventional (non-sustainable) loans to increase; they also anticipate that conventional loans will come with less favourable terms and conditions and/or that fewer conventional loans will be granted. Potential for improvement is seen when it comes to public support programmes.

2.2 Political framework

The EU’s Sustainable Finance Action Plan sets out ten initiatives. Overall, the action plan significantly advances the codification of sustainability in the financial sector. The measures fleshed out so far primarily use soft regulatory approaches based on information, transparency and standardisation. The Association of German Banks is monitoring the regulatory process and will continue to do so in the future with the aim of ensuring that regulation is designed to be fit for purpose.

Measures

In July 2021, the European Commission published its long-awaited revision of its sustainable finance strategy. The German government had already set out a national sustainable finance strategy in April 2021. The European Commission places particular emphasis on closing the remaining gaps between various legislative initiatives, ensuring greater consistency in legislation and pressing ahead with the implementation of measures. The centrepiece of the EU action plan, the taxonomy of sustainable economic activities, is to be finalised, for example. A positive step is that small companies are to receive more support in the area of sustainability. For banks, it is important that the framework is practicable to implement and not overly complex.

Greater consistency in the application deadlines of the legislative projects will be especially important. Proportional rules are also needed so that even more companies will sign up to the transformation process.

Outlook

The sustainable finance framework has largely been established at EU level, even if inconsistencies between individual legislative initiatives remain and further details need to be fleshed out at level 2. It is now up to the banks to implement the requirements and it is very much to be hoped that the European Commission will grant sufficient testing and learning periods before developing and launching further initiatives. Banks and businesses need time for implementation and for collecting data and making them available. In the interests of a good outcome, quality should take precedence over quantity. This should be reflected in the deadlines for applying the new rules.

It will be increasingly important not only to support companies that are already sustainable but to help businesses that are just starting their journey towards more sustainability. Small and medium-sized enterprises must be encouraged along

the path of transformation.

2.3 ESG risks

There is widespread consensus among regulators and supervisors that sustainability risks could become significant in scale, potentially posing a threat to the system. Their declared goal is to mitigate these risks.

Measures

The guidelines already issued by BaFin and the ECB on dealing with climate risks have high expectations of the financial sector. The task of the banks is now to develop corresponding solutions. The European Banking Authority (EBA) also published a report on ESG risks in the middle of this year. It is a substantial document and presents a balanced view of the current status of discussions, outlines possible strategies, and also identifies challenges and limitations.

At the Association of German Banks, we take the view that it is important to draw a clearer distinction with respect to ESG risks between objectives (solvency, strategic view) and different time horizons (short/medium to long term) and believe this is crucial when it comes to choosing the most suitable methodology. It should be borne in mind that there is a high degree of uncertainty, especially around long-term developments, so that risks can only be exactly quantified to a limited extent.

The Network for Greening the Financial System (NGFS), which now comprises 95 supervisory authorities and central banks, has refined its climate scenarios for the financial sector and increased their granularity. These scenarios will be the basis for the ECB’s 2022 climate stress test, for which the ECB is currently preparing a methodology in consultation with the institutions it supervises. The results of the stress test are intended to identify vulnerabilities of institutions; they should not serve as a starting point for deriving capital requirements – the scenarios contain too many assumptions and uncertainties for that.

Our association is collaborating with member banks of all sizes on finding sound solutions for identifying, measuring and managing ESG risks appropriately. Here, too, transparency is an important issue: we have put together a document providing a clear overview of the key points of the BaFin and ECB guidance.

Outlook

Based on its report, the EBA will develop concrete regulatory proposals. In the Capital Requirements Regulation (CRR) and the Capital Requirements Directive (CRD), the major pieces of EU legislation for banks, requirements concerning risk management and the supervisory review and evaluation process (SREP) will be amended to include ESG risks in the course of implementing Basel IV. By the end of 2023 at the latest, the EBA will announce whether “green” or “brown” assets should be accorded special treatment under supervisory law. The Association of German Banks has long advocated that supervisory law should give privileged treatment to sustainable finance with the aim of setting positive incentives for businesses and banks. Such treatment would be justified from a risk perspective since sustainable financing is by its very nature likely to carry lower ESG risks.

In 2022, the ECB will take a closer look at the implementation of its guidance by banks. Even if BaFin is not yet planning to review the implementation of its guidelines in 2022, Germany’s small and medium-sized institutions will, like its big banks, continue to work on the best ways of dealing with ESG risks. For one thing is clear: this is a new issue which still requires a lot of conceptual work. The Association of German Banks will offer its member banks strong support in the form of information and opportunities to exchange experience and views.

2.4 EU taxonomy of sustainable economic activities

The EU taxonomy is a system for classifying sustainable economic activities. It offers a common “language” for defining what in future can be considered environmentally sustainable.

Measures

The year 2021 marks a milestone in terms of operationalising the taxonomy: the technical screening criteria for the first two EU environmental objectives, namely climate change mitigation and climate change adaptation, were adopted in April in a delegated act. This now provides guidance for interpreting the highly complex framework. It is nevertheless often difficult for banks to check the screening criteria since the availability and reliability of data on many criteria can be problematic. At the beginning of July, the European Commission adopted taxonomy transparency obligations for banks. Banks now know how they have to calculate the new “green asset ratio” (GAR) for disclosing to what extent their portfolios qualify as sustainable in accordance with the taxonomy – although certain key application issues remain open. Our association successfully lobbied the European Commission for more appropriate transitional periods to allow banks to familiarise themselves with the new requirements and adjust e.g. their IT systems accordingly.

Outlook

The GAR will probably become extremely important. Its calculation is highly complex, so it would be appropriate to take a differentiated view. Banks with a lower green asset ratio will not always be less sustainable. Initial disclosures are expected next year and will begin by reporting and contextualising the taxonomy eligible activities. The green asset ratio will show how banks have integrated the taxonomy into their business processes. It is likely to be a demanding process.

The European Commission has set up a Platform on Sustainable Finance to make proposals for finalising the taxonomy. By early September, it had consulted on initial reports and plans for a social taxonomy and a potential extension of the taxonomy. The extension is intended to show how transition finance could be better reflected. Towards the end of the year, the European Commission is expected to launch a consultation on further technical screening criteria. The basic structure of the taxonomy is thus in place. The taxonomy remains a living document which will adapt to future developments in areas such as climate policy. How to ultimately implement the overall system in a practicable manner is still an open question and remains a challenge.

2.5 Sustainability reporting

Sustainability is one of the mega-issues of our time – and rightly so. Society’s expectations are rising that companies will behave responsibly. Companies above a certain size – including banks – are required to publicly report on their strategies and measures in areas such as environmental protection, treatment of employees, social matters, human rights and anticorruption.

Measures

On 21 April 2021, the European Commission unveiled its proposals to amend the Non-financial Reporting Directive (NFRD). Standards for corporate reporting on sustainability remain fragmented. Despite a number of frameworks, rules and regulations, there is a lack of comparable data for a thorough evaluation of sustainability. The revised NFRD will be renamed the Corporate Sustainability Reporting Directive (CSRD) and will establish a standardised reporting framework. This is absolutely necessary and very welcome.

But the consolidation of existing reporting standards should take place at international level: globally active banks and businesses need global standards.

Outlook

The CSRD envisages that European sustainability reporting standards will be developed by the European Financial Reporting Advisory Group (EFRAG). Companies will be required to publish their sustainability report in an electronic format. But the proposed timetable for these changes is overly ambitious, in our view. Businesses and banks will need considerably more time for their implementation – the time and effort required to implement the European Single Electronic Format (ESEF), for example, should not be underestimated. This is the only way to ensure that entities can deliver high-quality data.

At international level, an International Sustainability Standards Board (ISSB) is being set up under the auspices of the IFRS Foundation to develop international standards in the area of sustainability reporting.

2.6 Sustainable Finance Disclosure Regulation

The Sustainable Finance Disclosure Regulation ((EU) 2019/2088 – SFDR) regulates the disclosure of sustainability-related information in the financial services sector. Aspects of the regulation are fleshed out in detail by corresponding regulatory technical standards (SFDR RTS).

Measures

The regulation has applied to financial market participants and financial advisers since March 2021. It specifies how to make available information on sustainability in terms of the environmental, social and governance (ESG) characteristics of financial products. It also requires the disclosure of information about the integration of sustainability risks and the consideration of adverse sustainability impacts on processes and services.

The SFDR identifies two types of sustainable financial product, known as Article 8 and Article 9 products. Since it was already clear when the regulation became applicable that there were a number of open questions with respect to implementation, BaFin has issued guidance on which measures the market should implement for the time being until the SFDR RTS take effect.

Outlook

Detailed regulatory technical standards are being developed to flesh out the SFDR. Originally, these were supposed to become applicable on 10 March 2021 at the same time as the SFDR. But since the European supervisory authorities EBA, ESMA and EIOPA (collectively known as the “ESAs”) were late in submitting their draft standards, the European Commission decided to postpone their introduction until 1 January 2022.

As some sections of the RTS are still in the process of being revised, the Commission has now decided to push back their applicability by another six months to 1 July 2022. A positive aspect to come out of the delay is that there is now more time for implementation. There is nevertheless also some uncertainty surrounding how certain standards should be implemented since the content of certain adjustments has yet to be finalised. A related problem is the challenge of having all relevant data available before the standards finally become applicable.

In addition, further adjustments to the SFDR RTS will be needed when the environmental taxonomy is expanded and the social taxonomy is subsequently introduced.

2.7 MiFID II delegated acts

The revised MiFID II delegated acts introduce the consideration of sustainability preferences. Banks will in future be required to ask clients about their sustainability preferences when providing investment advice and portfolio management services and to take these preferences into account when recommending and selecting financial products.

Measures

The final version of the MiFID II delegated acts, published in April 2021, establishes three new product categories, which differ from and expand the range of Article 8 and Article 9 products under the SFDR. In addition to products that make a positive contribution under the Taxonomy Regulation and the SFDR (see Article 2(7)(a) and (b) of the MiFID II Delegated Regulation), a third category has been created that either qualitatively or quantitively considers principal adverse impacts (PAIs).

This will require a major adjustment to a joint standard developed by the German Banking Industry Committee (GBIC), the German Derivatives Association (DDV) and the German Investment Funds Association (BVI). The common minimum standard for the identification of a target market for securities will be extended to include ESG criteria.

Outlook

The revised standard is currently the subject of internal consultation among the associations and is expected to be finalised in autumn 2021. This will give financial institutions sufficient time for implementation. The challenge nevertheless remains of conducting extensive customer surveys on sustainability preferences from 2022 and of defining and selecting products on the basis of the new categories. All the more so given the continuing lack of available data.

2.8 Green Bond Standard

The EU has published a proposal for a European Green Bond Standard (EU-GBS) with the aim of mobilising green capital for the transition to a climate-neutral economy. The EU-GBS is intended to enable issuers to demonstrate that green projects financed by the bond comply with the EU taxonomy. This will make it easier for investors to assess the sustainability of their investment.

Measures

The Commission’s legislative proposal sets out the key features of the EU-GBS. First of all, the EU-GBS will be a voluntary standard, so the application of other recognised green bond market standards will still be possible. The EU-GBS requires the proceeds generated by green bonds to be fully channelled into projects that comply with the EU taxonomy. Detailed requirements to disclose how the proceeds of a bond will be used are intended to create transparency. To ensure compliance with the EU-GBS Regulation and conformity with the taxonomy, green bonds will have to be externally reviewed by reviewers supervised by the European Securities and Markets Authority (ESMA).

Outlook

In addition to the fact that application of the standard will be voluntary, a further positive aspect is that the proposed regulation envisages grandfathering arrangements for bonds issued prior to a change to the EU taxonomy, which is subject to a process of ongoing adjustment. The linking of activities to the EU taxonomy is an important step towards further standardisation, though this could initially pose a challenge. It remains to be seen to what extent the detailed requirements concerning the documentation

of bond issues will have an impact on banks.

2.9 Social aspects of sustainability

Interest in social aspects of sustainable finance has risen significantly in recent months. A number of regulatory measures are increasingly focusing on this aspect.

Measures

At EU level, a sustainable corporate governance initiative is planned for end of 2021. In Germany, the Bundestag passed the Supply Chain Due Diligence Act in June 2021. The regulatory framework for greater consideration of social aspects, especially human rights due diligence obligations for banks, will be expanded further.

The EU taxonomy will probably be extended to include a social taxonomy. It would be desirable to create a readily understandable overall system consisting of both green and social taxonomies. Although there is as yet no uniform definition of what constitutes “social”, criteria and categories have already been defined for instruments such as social bonds, which offers a good point of orientation.

Outlook

For banks, social equilibrium, the protection of human rights and sustainable corporate governance rank alongside environmental and climate protection issues in representing an important step towards greater overall economic sustainability. Many banks already base their activities on the widely recognised United Nations Guiding Principles on Business and Human Rights. The private banks believe that upcoming legislative initiatives should more strongly reflect the regulatory framework of banks. The Association of German Banks is committed to encouraging all its members to accompany it on the journey towards sustainable finance. A webinar was held to support banks that have not yet been able to address human rights issues in depth. Our association will continue to engage with this topic in the future.

3. Outlook

The private banks will continue to be proactive in tackling the issue of sustainable finance and the Association of German Banks will support its members in the process.

We welcome the opportunity for discussion with policymakers, businesses and civil society. Irrespective of the commitment of private banks, the financial sector will be subject to further regulatory measures.

The practical design of such regulation will be instrumental in determining whether financial market participants view sustainability as a bureaucratic burden or continue to see it as an opportunity to successfully manage the transformation of the economy in partnership with their customers.

As at September 2021

[1] German companies back Brussels climate mitigation policy (in German)

[2] Sustainable finance – the contribution of private banks – Association of German Banks

[3] The boxes in subsequent sections give examples of what private banks are doing in practice. They are inspired by individual banks but do not represent an exhaustive list of the strategies and activities being implemented by the private banks.